Buying a House in a Tier 1 City: Smart or Not?

September 26, 2025

For many, buying a house in a Tier 1 city like Mumbai, Delhi, Bangalore, or Hyderabad feels like the ultimate life milestone. It represents stability, security, and social status. Families often encourage it, and society tends to celebrate those who “settle down” with property ownership. Beyond the emotions, the appeal is also practical, better infrastructure, access to jobs, schools, and healthcare, and the promise of long-term appreciation. On paper, it looks like the smartest move one can make.

Harsh Reality

The problem is the numbers don’t always support the dream. In Mumbai, a modest 2BHK can easily cost ₹2–3 crores. With a 20-year loan, that translates into EMIs of ₹1.5–2 lakhs every month. For most people, that’s a huge financial burden. It leaves little room for other goals like travel, investments, or retirement savings. Renting tells a different story. The same ₹2 crore house might rent for just ₹50,000 a month, far lower than the cost of ownership. That gap makes you question whether buying is truly a smart financial choice.

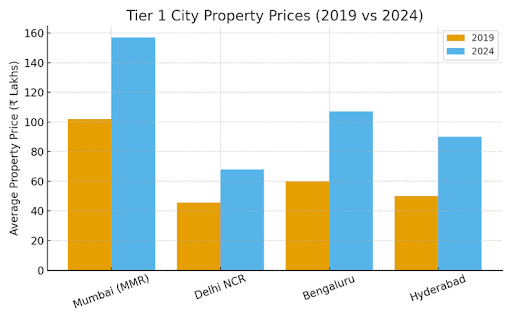

Realty Prices: How Much Have They Risen?

The numbers tell their own story. In Mumbai, the average home cost has jumped from around ₹1.02 crore in 2021 to nearly ₹1.57 crore in 2025, a rise of more than 50% in just four years. Bengaluru leads the pack with almost 78% appreciation in the last five years, while Delhi NCR and Hyderabad have also recorded sharp increases. This steady rise highlights why Tier 1 housing is both aspirational and financially challenging. While demand ensures prices rarely fall, the steep climb also makes affordability a serious concern for first-time buyers.

When Buying Makes Sense

Owning a home in a metro is not always a bad idea. If you’re settled in one city for the long term, buying provides stability. Property values in Tier 1 cities often rise over time due to limited land and strong demand, making it a relatively safe asset. If your finances are strong enough and EMIs don’t consume more than a third of your income, ownership can be a comfortable and even rewarding decision. There’s also the rental advantage. Even if you move later, a house in a metro can fetch strong rental returns.

When Buying Isn’t Smart

On the other hand, buying a house in a Tier 1 city can easily turn into a trap. The financial strain of a massive EMI can tie you down for decades. Many end up “house-rich but cash-poor,” where most of their income is locked into their home, leaving little flexibility for anything else. The opportunity cost is also significant. The same amount invested in mutual funds, digital gold, or even properties in Tier 2 and Tier 3 cities could yield better returns. And with careers becoming increasingly mobile, locking yourself into one city may limit your opportunities.

Smarter Alternatives

For many, renting in a Tier 1 city while investing elsewhere is a smarter approach. Renting allows you to enjoy the lifestyle of a metro without the burden of a massive loan. The money saved can be invested in diversified assets, creating wealth over time. Others choose to buy in smaller cities where property prices are affordable and infrastructure is rapidly improving. Some even prefer to delay the purchase entirely, focusing on building wealth first and buying later when it won’t strain their lifestyle.

The Verdict

So, is buying a house in a Tier 1 city smart or not? The truth is, it depends. It’s smart if you are financially comfortable, plan to stay in one city for the long haul, and value stability. But if the purchase forces you into financial stress, limits your flexibility, or prevents you from investing in other opportunities, it may not be the best move.

The smarter question to ask yourself is this: Will this house support my goals, or will it restrict them? If ownership feels like a limitation, then renting and investing may be the wiser path. After all, financial freedom often matters more than the status of ownership.

Ria Jadav

September 26, 2025

Latest Blogs

No blogs available.